Inflation continues its slow decline in the euro area. According to Eurostat’s rapid estimate, consumer prices rose by 2.5% in June, compared with 2.6% in May.

While the increase in food prices is in line with the main index, energy prices did not increase by 0.2% year-on-year. On the other hand, the price of services rose by 4.1% in June (as in May), the strongest increase since October 2023.

This will not reassure Christine Lagarde and her colleagues at the European Central Bank, even if the general index remains well oriented. This figure should not change the current trend: the ECB should lower its rates again after the summer, probably once or twice. While the minutes of its policy meeting indicate that the June decline was not consensual, the latest PMI indices that measure economic activity point to an economy that is clearly slowing, with the HCOB Eurozone Composite at 50, only 9 points in June compared to 52.2 points in May and a manufacturing sector that is falling back (only 14.8 points).

This underscores that the risks to the economy remain significant. Despite slowing activity, Brent’s barrel is currently hovering around 87USD. While it ended May at around 81USD. At the same time, the various States are gradually reducing (costly) subsidies that have reduced the impact of energy prices on the private sector. Energy prices may not have had the last word.

Second, we must keep in mind that given the high debt and financing needs continue to increase (in Europe as well as in the United States) while central banks, which have long been the buyer of last resort of sovereign debt, gradually withdraw from these markets. Competition between the two regions is likely to intensify and, with the United States offering yields well above those of the eurozone, it is likely that bond yields in the eurozone will have a hard time falling by much, even if the ECB lowers its key rates again, as investors think.

France: towards a total deadlock

While the British have offered their new government a large majority, which will allow them to govern with stability in the coming years, France has chosen a completely different path, on June 7.

The barrier evoked against the RN of Le Pen and Bardella worked well, the latter finishing only 3rd among the large blocks.

But beyond that, it is clear that the clarification that President Macron wanted did not take place and that no one knows where the country is going.

After the election, no party has a majority and possible coalitions are extremely difficult. Winner of the election, the New Popular Front does not have a majority and will have to find agreements with others. However, if the left parties that constitute it agree to block the RN, they disagree on many other issues. Trade-offs will therefore be difficult, especially since some of the proposed measures would be very costly. Repeal of the pension law (one of the few serious reforms carried out by E. Macron), increase of the minimum wage and social spending of all kinds, capping energy prices, increase of the tax burden on companies, the programme is not likely to improve the business climate in France or to give confidence to debt markets.

Fortunately for them, it has little chance of passing and France is probably going towards a period of blockages and immobility that will last… until the presidential election of 2027, in all probability.

Markets have reacted little but remain nervous. This makes sense because by 2027, significant public account deficits are expected, because if there is no majority to increase spending, there will be no majority to reduce spending. This should put pressure on the French debt and its differential against the German debt.

With the Berlin government struggling, too, Europe is heading for a long period of weakness. At a time when it is little heard on the world stage, and is falling behind in the sectors of the future, it needs clear policies and a long-term vision. That’s not the way she’s going.

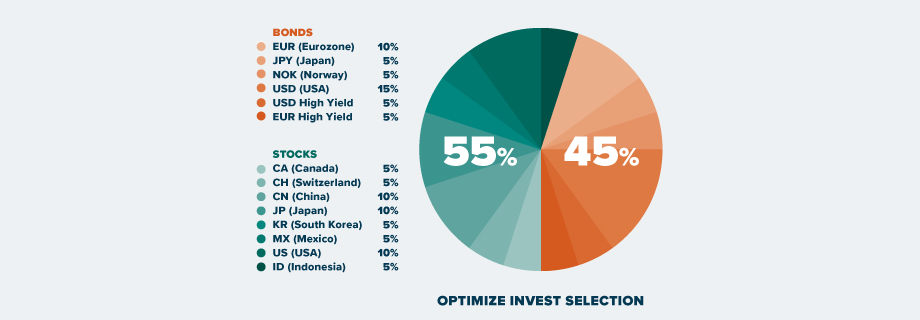

We only invest in the euro area through individual equities.