The report of the last policy meeting of the US Federal Reserve reassured investors.

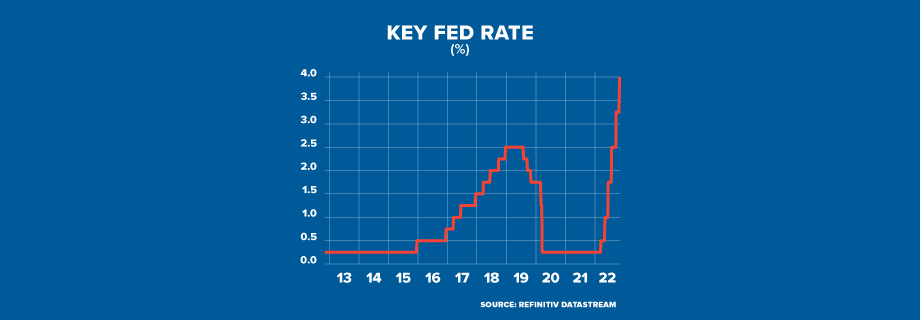

After four policy rate hikes of 0.75% in June, July, September and November, most members of the Monetary Policy Committee are leaning towards a slowdown in the pace of increases.

Therefore, investors started to bet on a 0.5% rise at the December meeting and hope for a turning point in US monetary policy.

However, the same report indicates that key interest rates could finally peak at a level slightly higher than expected in the latest projections (4.6%), which date from September. But markets have chosen to see the glass half full, and financial assets everywhere have benefited.

This is the case since the announced end of the 0.75% increases allowed the US dollar to return to the ground, reaching peaks against many currencies in recent months.

The fall in bond yields in the United States has allowed many other bond markets to make up some yield differentials that separate them from the American market, supporting their currencies.

The high cost of the USD has contributed significantly to the high inflation experienced by many countries. As commodity prices are denominated in this currency, the expensive dollar strengthens its price rise for other consumers whose currency is depreciating. A weaker U.S. dollar is a relief for many economies.

Once inflation is controlled, the American economy has all the conditions to get back on its feet.

We continually invest in them as part of our diversified portfolios.