Global Macro Outlook for 2026 Second Half

The first half of 2026 was dominated by two key themes: war and artificial intelligence. Investors had initially expected falling inflation and interest rate cuts globally, supporting moderate growth. Instead, the conflict in the Middle East and the closure of the Strait of Hormuz disrupted energy supplies, pushing oil and gas prices higher and reigniting inflation.

US inflation rose from 2.4% to 4.2%, while Eurozone inflation doubled to 3.2%. As a result, expectations for monetary easing reversed, bond yields increased, and central banks shifted back toward tighter policy.

Financial Markets vs Real Economy Divergence

Despite weaker real-economy conditions—driven by higher inflation, tighter credit, and weakening consumer confidence—equity markets continued to rise. Strong corporate earnings and the AI investment boom, led by companies such as Nvidia, supported global indices, pushing markets to new highs in the US and parts of Asia. However, rising rates create challenges for financing the massive infrastructure needs of AI and data centres.

Looking ahead, geopolitical developments remain crucial. A potential US–Iran agreement could ease tensions in the Middle East and normalize energy flows, reducing inflationary pressure and supporting consumer confidence and markets. If it fails, the current status quo is likely to persist, with continued volatility but no major structural change.

US Market Outlook: AI, Innovation and Global Capital Dominance

In the US, market leadership is broadening beyond the “Magnificent 7” (Apple, Microsoft, Amazon, Google, Meta, Tesla, Nvidia). New sectors such as infrastructure, space, quantum computing, and defense are gaining importance, and more companies are entering the trillion-dollar club. The US market continues to stand out due to its scale, innovation, and ability to attract global capital, making it increasingly difficult to avoid for investors.

Asia Market Outlook: Taiwan, South Korea and Japan Tech Boom

In Asia, tech-driven growth remains strong, particularly in Taiwan, South Korea, and Japan, where semiconductor and AI-related companies dominate indices. However, underlying economies face challenges from high energy costs, tariffs, and Chinese competition. While valuations in some markets are reasonable, high valuations in AI leaders raise concerns about overheating.

Eurozone Outlook: Weak Growth and Structural Challenges

Europe continues to lag, with limited tech leadership and dependence on external demand, particularly luxury goods and Chinese consumers. Growth remains weak, and higher interest rates add pressure. Even with improved energy conditions, Eurozone growth is expected to remain modest. The UK faces fiscal constraints, while Sweden shows more innovation potential. Poland remains the preferred European market due to strong domestic demand and EU fund inflows.

China Outlook: AI Competition and Export Strength

China presents a strategic uncertainty. It is highly competitive in AI but focuses on low-cost, broad-based productivity gains rather than profit-driven innovation. Its export strength continues, but domestic demand remains weak and growth targets are modest. The global AI competition between US and Chinese models could have major implications for technology leadership and valuations worldwide.

Emerging Markets Outlook: Mixed Performance

Emerging markets have been mixed. India and Indonesia were hurt by higher energy prices and governance concerns, particularly in Indonesia, where policy uncertainty has undermined investor confidence. In contrast, Brazil and Mexico performed better, supported by energy exports and macroeconomic stability. Brazil benefits from rising oil production and expected rate cuts, while Mexico remains closely tied to US supply chains, with steady but cautious growth outlook despite political uncertainty around trade negotiations.

Key Investment Themes for 2026 Second Half

The second half of 2026 is expected to be driven by:

- Geopolitical risk in the Middle East

- Energy price normalization (or continued volatility)

- AI-driven equity market expansion

- Diverging global growth across regions

- Structural dominance of US technology markets

Conclusion: A Market Defined by AI and Geopolitics

Overall, the second half of 2026 will largely depend on geopolitical developments and the evolution of the AI investment cycle, with continued US dominance, selective opportunities in Asia and emerging markets, and structurally weaker conditions in Europe.

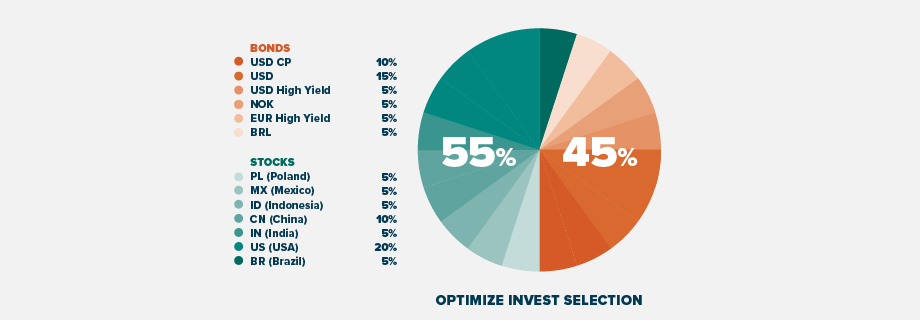

See below our recommended portfolio, this Optimize Invest Selection illustrates the base strategy associated with a moderate risk profile, within a broader set of approaches designed for different investor profiles.

For more information about the fund characteristics, terms and conditions, and factsheet visit https://optimize.pt/en/investment-funds/invest-selection/