For several months, investors had grown accustomed to the prospect of persistently high inflation. The appointment of Federal Reserve President Kevin Warsh fuelled speculation that the Fed might tolerate higher inflation, raising questions about the central bank's independence and its commitment to price stability. At the same time, central banks continued increasing their gold reserves, prompting renewed debate over the long-term role of the US dollar as the world's primary reserve currency. The disruption to Gulf oil production during the conflict also led some commentators to question the future of the petrodollar system.

Those concerns have since moderated. In his inaugural speech, Warsh reaffirmed the Federal Reserve's commitment to controlling inflation and made clear that interest rates would be raised if necessary to preserve price stability. As confidence in the Fed recovered, expectations of a prolonged inflation shock also faded.

Importantly, the Fed may not need to tighten monetary policy further. As shipping through the Strait of Hormuz gradually resumed, oil prices quickly returned to pre-conflict levels, easing inflationary pressures — particularly in the United States. With hindsight, the Fed's decision to wait before adjusting rates appears more measured than the European Central Bank's immediate rate hike.

US dollar strengthens as confidence returns

The shift in expectations has produced two notable market developments.

First, the US dollar has strengthened against the euro, trading between 1.13 and 1.14 — its strongest level in more than a year.

Second, the US equity market continues to offer investors broad and diversified opportunities. Supported by global leadership in artificial intelligence, technology and innovation, the United States remains one of the most attractive investment destinations despite recent volatility.

China faces slowing domestic demand

China has been among the weaker-performing major markets over the past month.

Domestic demand continues to disappoint, with the anticipated recovery in consumer spending and private-sector activity failing to gain momentum. At the same time, Beijing has introduced new export restrictions on selected rare earth minerals and strategic materials. While intended to strengthen China's strategic position, these measures could weigh on export growth, one of the country's principal economic drivers.

Brazil balances inflation risks and election uncertainty

Brazil has also struggled to maintain recent market momentum.

Although the Central Bank of Brazil has reduced the Selic rate three times during 2026, the benchmark rate remains elevated at 14.25%. Additional cuts would help reduce borrowing costs and stimulate domestic demand, but inflation remains at 4.7%, above the central bank's 4.5% tolerance ceiling. As a result, policymakers have limited room for further monetary easing.

Investors are also watching the upcoming general election later this year, adding another layer of uncertainty. Consequently, after several months of strong performance, the Bovespa has entered a period of consolidation. Nevertheless, Brazil continues to offer attractive medium- and long-term investment opportunities for investors willing to tolerate short-term volatility.

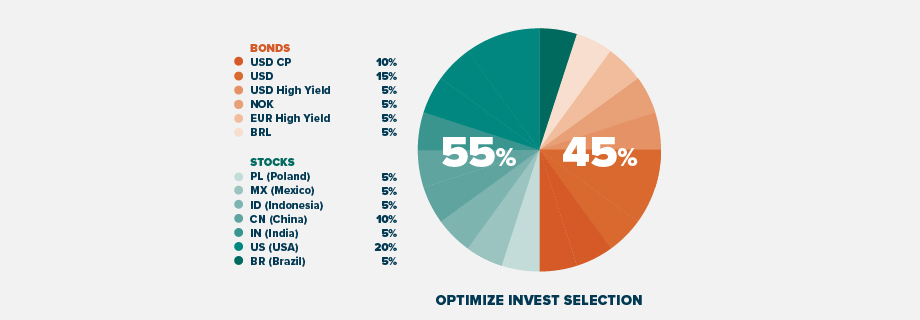

A Balanced Strategy for an Unbalanced World

With uncertainty persisting across markets, diversification remains one of the most effective ways to manage risk. A balanced portfolio such as Optimize Invest Selection combining equities and bonds seeks to capture long-term growth opportunities while helping cushion periods of market volatility.

For more information about the fund characteristics, terms and conditions, and factsheet visit https://optimize.pt/en/investment-funds/invest-selection/